Recent Blue Posts

Recent Blue Posts

Feedback: Death Knight Updates

Feedback: Death Knight Updates Feedback: Death Knight Updates

Feedback: Death Knight Updates Season of Discovery - Class Changes Feedback

Season of Discovery - Class Changes Feedback Filter options for non retail wow content

Filter options for non retail wow content MMO-Champion

MMO-Champion

No, say you have 1% cash back and no interest for a few months...Originally Posted by Unionoob

If you buy something that costs $10,000 with it and pay back that $10,000 before any interest accrues, you paid just as much as you otherwise would have paid and got a free $100 from your 1% cash back.

Recent Forum Posts

Recent Forum Posts

View Poll Results: What's your FICO Score?

- Voters

- 54. This poll is closed

-

2017-07-19, 06:42 PM #21Titan

- Join Date

- Nov 2013

- Location

- Cincinnati, Ohio

- Posts

- 11,244

-

2017-07-19, 06:43 PM #22The Unstoppable Force

- Join Date

- Jan 2009

- Location

- Finland

- Posts

- 23,400

Such credit cards don't exist here. Originally Posted by melodramocracy

Originally Posted by derpkitteh

Originally Posted by derpkitteh

-

2017-07-19, 06:45 PM #23Brewmaster

- Join Date

- Jun 2009

- Posts

- 1,373

How is that making money? Then you paid same amount as you would have paid with with cash or Debt card.. Originally Posted by I Push Buttons

-

2017-07-19, 06:48 PM #24Brewmaster

- Join Date

- Jun 2009

- Posts

- 1,373

I am not sure from where is Puupi, but here where I live you only get 0% if you pay back 100% amount on next month. Originally Posted by Sulla

-

2017-07-19, 06:52 PM #25Titan

- Join Date

- Nov 2013

- Location

- Cincinnati, Ohio

- Posts

- 11,244

With regard to my example, did you get a free $100 paying cash? Originally Posted by Unionoob

-

2017-07-19, 07:02 PM #26The Unstoppable Force

- Join Date

- Nov 2010

- Posts

- 21,123

Because you just made 100 bucks. Originally Posted by Unionoob

Before the housing fallout several years back, you were seeing interest rates for some savings accounts hitting 5% or so. People who had extremely good credit (and usually owned a home) would practice credit card arbitage, which would mean they'd leverage as much credit as possible on 0% credit cards (typically balance xfer), throw all that money into a 5% account, wait almost the entire alloted time, then just pull out what they needed to pay off the cards.

If an emergency comes up before the 0% is due, you just pay if off early. This doesn't sound like a ton of money, but 5% guaranteed on 100k or so becomes rather worthwhile.

You don't see it happening now, because interest rates make saving money generally pointless.

More reading: https://www.thepennyhoarder.com/smar...ard-arbitrage/

-

2017-07-19, 07:06 PM #27I am Murloc!

- Join Date

- Oct 2010

- Location

- 20 Miles to Texas, 25 to Hell

- Posts

- 5,802

Check back in June. Only been building credit for five years.

-

2017-07-19, 07:16 PM #28Void Lord

- Join Date

- May 2011

- Location

- In Security Watching...

- Posts

- 43,744

Why did drop and how did you bring it back up. Originally Posted by Forgettable

Milli Vanilli, Bigger than Elvis

Milli Vanilli, Bigger than Elvis

-

2017-07-19, 07:18 PM #29Immortal

- Join Date

- Aug 2010

- Posts

- 7,489

Presumably it dropped because after buying a house his ratio of credit used vs. credit available was much lower, and it went up because he paid off more of the mortgage. Originally Posted by Mall Security

-

2017-07-19, 07:20 PM #30The Forgettable

- Join Date

- May 2010

- Location

- Calgary, Canada

- Posts

- 5,180

Yea, this. Originally Posted by DarkTZeratul

-

2017-07-19, 07:21 PM #31Void Lord

- Join Date

- May 2011

- Location

- In Security Watching...

- Posts

- 43,744

Not a dick measuring contest. Credit is important and it's something people don't talk about enough and everyone can learn from each other. My credit isnt perfect and I struggled more in the beginning and have bumps now. Learning from others could be helpful. Originally Posted by Akka

Milli Vanilli, Bigger than Elvis

-

2017-07-19, 07:24 PM #32I am Murloc!

- Join Date

- Mar 2012

- Location

- Zebes, SR-21

- Posts

- 5,886

One of the easiest ways to build credit it to get a credit card (or two) and use them to pay off the entirety of your bills, then immediately go and pay off the credit cards with your bank balance. If you do it quick you don't accrue interest, and it looks great on your credit history (putting a large balance on it every month, and then paying it off in full)

-

2017-07-19, 07:24 PM #33Void Lord

- Join Date

- May 2011

- Location

- In Security Watching...

- Posts

- 43,744

Gotcha I paid mine off and cars so I've never taken a hit like that but never been near 800. Interesting information you posted. Originally Posted by DarkTZeratul

Milli Vanilli, Bigger than Elvis

-

2017-07-19, 07:24 PM #34The Undying

- Join Date

- Nov 2015

- Posts

- 32,577

I wonder about that... Originally Posted by DarkTZeratul

Credit scores are a double edged sword. I tend to view them as how much am I being suckered into borrowing money at such interest rates.

That being said , if a person wants a high interest score just make sure you pay at the very least the monthly minimum ON TIME.

I just as soon pay cash or do without. (Not realistic, I know)

-

2017-07-19, 07:25 PM #35Banned

- Join Date

- Dec 2009

- Location

- US

- Posts

- 23,727

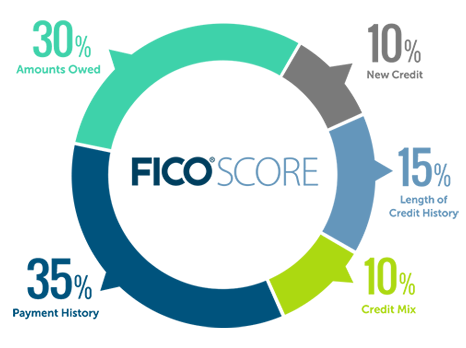

Your fico score depends on what model they are using. Some places use FICO 8 which will give you a better score but banks will use FICO 2 or 4 depending on the credit agency, it can easily be a 100 point swing. Enjoy! Originally Posted by Mall Security

-

2017-07-19, 07:28 PM #36Void Lord

- Join Date

- May 2011

- Location

- In Security Watching...

- Posts

- 43,744

I do this now and have no debt, but some I know say having no debt can lower a persons score. Originally Posted by Phookah

- - - Updated - - -

Originally Posted by zenkai

Interesting also surprised it can dip too.Milli Vanilli, Bigger than Elvis

-

2017-07-19, 07:31 PM #37Legendary!

- Join Date

- Sep 2008

- Posts

- 6,543

Yeah yeah, sure, "post your number" on a forum is certainly not a dick-waving contest... Originally Posted by Mall Security

-

2017-07-19, 07:33 PM #38Void Lord

- Join Date

- May 2011

- Location

- In Security Watching...

- Posts

- 43,744

Yep this is the conclusion I've come to also. Have a friend born into wealth never had debt and millions even his score Isn't 800. That's weird as hell to me. Originally Posted by Shadowferal

Milli Vanilli, Bigger than Elvis

-

2017-07-19, 07:37 PM #39The Patient

- Join Date

- Nov 2016

- Posts

- 286

670.

Kinda sucks but that was up from about 620 a couple of years ago. I was in a very bad place financially, underemployed with a family and I needed to put budget overruns on my credit balance.

My tips for rasing your score:

Use credit cards for all necessities where you can to build credit and get cash back. Use cash back directly on your balance.

Put your cards on auto pay for the minimum. That way if you forget to make a payment you'll be covered.

Limit your spending as much as possible and put as much down on your debt as you can every paycheck (make sure you set aside enough for rent and utilities)

Keep a running ledger of expenses so you can see where cash is going at any given point.

After you get 2-3 good cards don't apply for anymore. The credit checks generally aren't worth it.

Every 6 months or so try for a credit line increase, BUT only if your card provider dose soft credit checks. If you need to authorize a credit check, don't do it, its usually not worth the hit unless you are VERY confident your Credit Line will increase.

Don't close credit accounts unless you absolutely have too. FICO takes into account length of credit history and if you shut an old one down that's a lot of history you're wiping.

Take every opportunity you can to make money, and put it down on your debt. Its hard to work and not treat yourself, but its better in the long run.

If your in a bind you can try to play the "closing dates" on your cards. The closing date is the only date where the balance on a card counts toward your credit score. Its usually 1-3 business days after your due date (check your individual statements and cardholder agreements) So if you need to carry a balance try to make big payments before the closing date, and then just build up the rest of the month again. You're credit will look much better even if there is no practical change in your financial situation.

-

2017-07-19, 08:04 PM #40Immortal

- Join Date

- Aug 2010

- Posts

- 7,489

A lack of debt will never lower your credit score, though never establishing debt in the first place can prevent it from increasing. Originally Posted by Mall Security

Reply With Quote

Reply With Quote