Yet another Timewalking loot post ( As directed by GM)

Yet another Timewalking loot post ( As directed by GM) Opened timewalking Cache before hotfix

Opened timewalking Cache before hotfix An Update on This Year’s BlizzCon and Blizzard’s 2024 Live Events

An Update on This Year’s BlizzCon and Blizzard’s 2024 Live Events Are we approaching a Solo Raid WoW Experience?

Are we approaching a Solo Raid WoW Experience? Void Elf starting pet?

Void Elf starting pet? MMO-Champion

MMO-Champion

If any Momentum chaps / chapettes / chap-gender-neutrals are reading, just to clarify:Originally Posted by Kallisto

Unless Labour come down from the fence, I will vote Tory.

I don't want to vote Tory, I hate my local Tory. But in the event of a GE called because May is ousted, unless Labour specifically come out in favour of a second referendum I will vote Tory. Because if we're going to hard Brexit, I'm sure as fuck not going to do it with a socialist government.

Thanks.

Recent Blue Posts

Recent Blue Posts

Recent Forum Posts

Recent Forum Posts

View Poll Results: 10 days left, what'll it be?

- Voters

- 92. This poll is closed

Thread: The Brexit aftermath thread

-

2018-11-10, 10:41 PM #8341Dreadlord

- Join Date

- Jun 2009

- Location

- Here lies David St. Hubbins, and why not?

- Posts

- 839

You can't really dust for vomit.

-

2018-11-10, 10:45 PM #8342Merely a Setback

- Join Date

- Feb 2009

- Posts

- 26,425

Why specifically? I mean, you're speaking about a major recession already. What's a socialist Government going to do to worsen then situation? You could literally put a monkey in the PM seat and it'd be just as dramatic. In other terms, when you drive your car down the cliff, does it really matter if you're sitting in a VW Beetle or a Ferrari F40? Originally Posted by Nigel Tufnel

Users with <20 posts and ignored shitposters are automatically invisible. Find out how to do that here and help clean up MMO-OT!

PSA: Being a volunteer is no excuse to make a shite job of it.

-

2018-11-10, 10:48 PM #8343Deletedwho did you vote for last general election/the one before? Originally Posted by Nigel Tufnel

-

2018-11-10, 10:50 PM #8344Dreadlord

- Join Date

- Jun 2009

- Location

- Here lies David St. Hubbins, and why not?

- Posts

- 839

I'm going to take this with a pinch of salt, dude. Originally Posted by Slant

GDP contracts, Labour spends

GDP contracts, Tories don't spend

Explain which is worse for me (higher rate tax payer)?You can't really dust for vomit.

-

2018-11-10, 10:52 PM #8345I am Murloc!

- Join Date

- Apr 2011

- Posts

- 5,021

Voting Tory because Labour isn't following the Brexit path you want is utterly ridiculous. It's like saying "I can't support Mussolini, he's too right wing for me. He needs to change otherwise I'm voting Hitler". Originally Posted by Nigel Tufnel

How would a Brexit under a Socialist government be worse than under this crew of self-serving idiots? Are you concerned they will keep the worker protections we've enjoyed under the EU, and you want to vote in a Tory government to make completely sure we get rid of them? You are going to have to explain this position you're taking, because from where I'm sitting it makes zero sense.When challenging a Kzin, a simple scream of rage is sufficient. You scream and you leap.

Originally Posted by George Carlin

Originally Posted by Douglas Adams

-

2018-11-10, 10:53 PM #8346The Lightbringer

- Join Date

- Apr 2011

- Posts

- 3,583

From what I can tell, it looks like Great Britain is in free fall, and everyone is trying to make sure they don't get blamed for what is about to happen. Probably the best possible result would be for everyone to yell "The SKY IS FALLING!!!", and then when things get bad, everyone can fall back on "Yeah, but it's not as bad as I thought it would be."

On the other hand, I have not heard too much of anything TRULY bad happening to the British economy. So maybe things will just muddle along. However, since both left wing and right wing politicians seem to be in duck and cover mode, I suspect that their private sources agree that the future does not look good for the country.

-

2018-11-10, 10:54 PM #8347Dreadlord

- Join Date

- Jun 2009

- Location

- Here lies David St. Hubbins, and why not?

- Posts

- 839

Last election: Lib Dem Originally Posted by ctd123

Election before: Lib Dem

EP elections: GreenYou can't really dust for vomit.

-

2018-11-10, 10:55 PM #8348The Lightbringer

- Join Date

- Apr 2011

- Posts

- 3,583

In practice, "not spending" extends recessions. The good news with a Tory government, in a recession, is that, without a job, your taxes will be VERY low. Originally Posted by Nigel Tufnel

-

2018-11-10, 10:58 PM #8349Dreadlord

- Join Date

- Jun 2009

- Location

- Here lies David St. Hubbins, and why not?

- Posts

- 839

Fuck me, this forum is populated by Keynesian economists Originally Posted by Omega10

- - - Updated - - -

Look chaps, chapettes, chap-gender-neturals...

I really don't want to get into an argument.

You should all know by now where I'm coming from.

You lot persuade Corbyn that I should vote for him and I will do.

Simple enoughYou can't really dust for vomit.

-

2018-11-11, 01:28 AM #8350The Lightbringer

- Join Date

- Jul 2014

- Location

- The Sunny Uplands

- Posts

- 3,825

You heard right. Here's the reason (thanks to the brexit vote).... Originally Posted by Omega10

The new quarterly GDP figures this morning reveal that EU economies are experiencing a significant slowdown in growth. The UK on the other hand is one of the few EU countries where GDP growth is higher this year than last year

Did you also not hear that the peoples (Germany) who are going to bankroll the EU from now on, instead of the UK, are about to release their latest figures in a few days time? Oh yes for sure they will be bad the only question is how bad will they be? And then there's the Italian revised budget due in to their EU masters on Tuesday...yeah right lolz dont hold your breath and in the meantime tick tock....13/11/2022 Sir Keir Starmer. "Brexit is safe in my hands, Let me be really clear about Brexit. There is no case for going back into the EU and no case for going into the single market or customs union. Freedom of movement is over"

-

2018-11-11, 02:18 AM #8351Over 9000!

- Join Date

- Mar 2014

- Posts

- 9,417

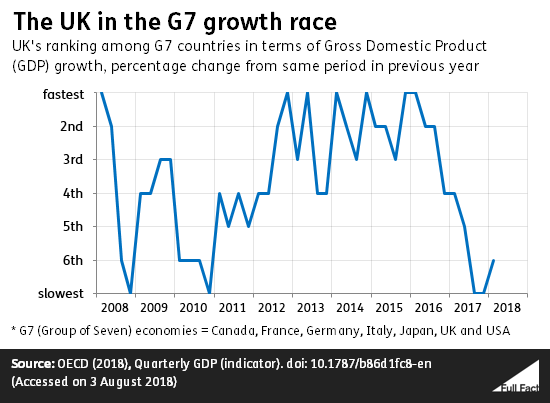

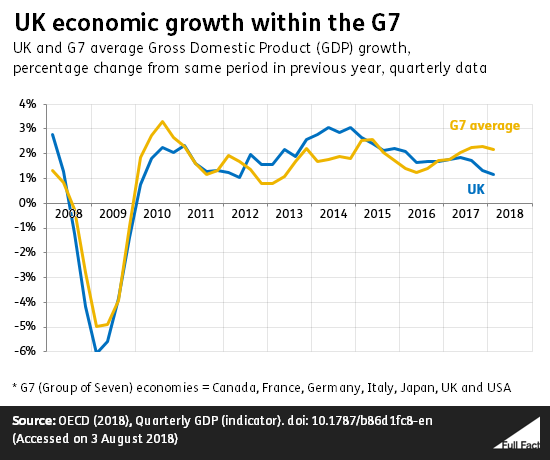

Oh Hi Dribbles and absolute lie of a chart. Shall we look at real numbers. Originally Posted by dribbles

https://fullfact.org/economy/uk-econ...wth-within-g7/

6th? tisk tisk that certainly doesn't put the UK above France or Germany. Also a nice drop that seems to happen about the same time a certain vote went ahead? Coincidence?

Uk well below G7 Average.

So even if one blip happens it's still 24+ months before that of a massive downward movement on the leaderboard. It's like basically being Bottom of the premier league losing non stop for a year, get relegated, then come bottom of championship, get relegated again and somehow celebrating a technicality win in the FA trophy first round against a non league side.

-

2018-11-11, 02:36 AM #8352Merely a Setback

- Join Date

- Feb 2009

- Posts

- 26,425

Just to illustrate the typical website this clown seems to visit... despite the political heavy weights of The Sun and The Express, this is the true nature of his agenda: Originally Posted by clownboat

https://order-order.com/2018/11/09/e...owth-slowdown/

Let's look at the graph, shall we? Notice how the HUGE COLUMNS are actually just .2 apart? Yeah, that's 0.2% difference. Wow, that's... incredible. Let's make those columns 10m high, every 2 metres, we'll make a line and call that a MASSIVE difference. You're so desperate grasping for straws...

Here's another chart:

And another.

You know what those charts show? They show that your little .2% massive WIN is actually less than half the usual seasonal fluctuation. This isn't a win for you clownboats, this is just... a fluctuation. And you're still in the EU. Your economy still works... somewhat, we're seeing the first kinks already, but that's just a sneak preview.

But let's see what actual economics have to say about this chart:

https://tradingeconomics.com/united-kingdom/gdp-growth

Yeah, great outlooks. God, I hope you'll have the balls to come back here in 1-2 years...The British economy grew by 0.6 percent on quarter in the three months to September 2018, following a 0.4 percent expansion in the previous period and matching market expectations, a preliminary estimate showed. It was the strongest growth rate since the last quarter of 2016 as household spending and exports rose firmly while business investment contracted at the fastest pace since early 2016 in part due to Brexit-related economic and political uncertainty.

Household consumption growth picked up to 0.5 percent in the third quarter from 0.4 percent in the previous three-month period. While the increase in Quarter 3 reflected growth across most categories of expenditure, there was a notably sharp drop in household spending on transport. In addition, government spending rebounded 0.6 percent after a 0.4 percent drop in the previous period; and net external demand contributed positively to the GDP growth as the trade deficit narrowed sharply to £1.655 billion from £5.659 billion in the previous period. Exports of goods and services jumped 2.7 percent (vs -2.2 percent in Q2) while imports were flat (vs -0.2 percent in Q2).

Meanwhile, the largest negative contribution to growth in Quarter 3 came from gross capital formation (GCF) – which includes gross fixed capital formation (GFCF), changes in inventories and acquisitions less disposal of valuables – subtracting 0.6 percentage points. However, this largely reflects the application of an alignment adjustment (used to balance the three approaches to measuring GDP) to the changes in inventories component. Still, GFCF rose 0.8 percent in the third quarter driven by a strong increase in government investment (8.6 percent), which was the strongest seen since Q1 2014 and reflects broad expenditure growth across central government, most notable in defence. The rises in government and private dwelling investment were partially offset by a 1.2 percent decrease in business investment in Quarter 3. This was the sharpest decline since Q1 2016 and marked the third consecutive quarterly fall – which has not been seen since the global financial crisis.

"However, today’s figures should be interpreted with some caution as early estimates of business investment can be prone to revision. The recent subdued business investment environment is consistent with external surveys of investment intentions, which attribute much of the weakness to Brexit-related economic and political uncertainty. The uncertainty appears to be deepening recently, with the latest Bank of England’s (BoE) November Inflation Report noting that Brexit and associated uncertainty “may have weighed on investment by more than had been expected in August”. The BoE’s Agents’ summary survey for Quarter 3 further indicated that Brexit uncertainty was the single largest factor weighing on firms’ investment spending plans. These sentiments are echoed in the latest Confederation of British Industry’s (CBI) Industrial Trends Survey (ITS) for the three months to October, which saw planned capital expenditure on plant and machinery for the year ahead fall at its fastest pace since July 2009." the Office for National Statistics said.

From the production side, construction output growth continued to pick up following a weak start to the year, while quarterly output in the manufacturing sector rose for the first time in 2018. Growth in services output slowed to 0.4 percent, but remained the largest positive contributor to GDP growth in the third quarter.Users with <20 posts and ignored shitposters are automatically invisible. Find out how to do that here and help clean up MMO-OT!

PSA: Being a volunteer is no excuse to make a shite job of it.

-

2018-11-11, 12:19 PM #8353The Lightbringer

- Join Date

- Jul 2014

- Location

- The Sunny Uplands

- Posts

- 3,825

You want economic heavyweights? How about.... Originally Posted by Dummkopf

UK GDP Growth Fastest In Nearly 2 Years

LONDON (Alliance News) - The UK economy expanded at the fastest pace in nearly two years in the third quarter driven by household spending and exports, despite heightened uncertainty over the Brexit deal.

http://www.morningstar.co.uk/uk/news...y-2-years.aspx

Got to love those exports. And...

Germany: More disappointments

September trade data adds to recent evidence of the worst quarterly performance for the German economy since 2015

https://think.ing.com/snaps/germany-...sappointments/

Didn't I always say Brexit would be worse for the EU than the UK? The only reason that graph has an x axis starting at 0 is because the latest GDP figures from Germany haven't been released yet...who knows the next graph may have to start with a negative on the x axis just to accommodate them. Bwaahhahahaaaa and you have an EU army to begin funding, more bwahahahaaaa

Considering much of those stockpiles would come from the EU, you sell more stuff to us than we to you (for now!), shouldn't the eurozone be booming rather than stagnating as a result of losing the UK cash cow? Originally Posted by Nymrohd

13/11/2022 Sir Keir Starmer. "Brexit is safe in my hands, Let me be really clear about Brexit. There is no case for going back into the EU and no case for going into the single market or customs union. Freedom of movement is over"

-

2018-11-11, 12:25 PM #8354Merely a Setback

- Join Date

- Feb 2009

- Posts

- 26,425

What a clown... here's a joke:

The Soviet Union and the US had a race once. The US won, naturally, and the SU came in second. That's how it was reported in the US. In the Soviet Union it was reported "The Soviet Union fought for a well earned 2nd place, while the US were second to last..."

That's what Dribbles does. He gets an orgasmatic excitement over... .2% growth and tries to sell it as the giant victory while ignoring the big recession that is looming ahead. Go ahead, clownboat. Celebrate this, go ahead... throw some konfetti. You earned it. A whole .2% increase above Germany. That'll be worth... wow, at least a couple million right? HahaUsers with <20 posts and ignored shitposters are automatically invisible. Find out how to do that here and help clean up MMO-OT!

PSA: Being a volunteer is no excuse to make a shite job of it.

-

2018-11-11, 01:03 PM #8355Banned

- Join Date

- Nov 2018

- Posts

- 24

The people spoke... it doesn't matter anymore if you believe they are correct or not the fact the plan seems to be to drag it out forever u till people vote the right way is disgraceful.

-

2018-11-11, 01:17 PM #8356The Unstoppable Force

- Join Date

- Feb 2008

- Location

- pending...

- Posts

- 23,968

Going out of Business Sales tend to bring in a good amount of revenue. They however also don't go on forever, for obvious reasons. Originally Posted by dribbles

Originally Posted by ash

Originally Posted by PC2

-

2018-11-11, 03:12 PM #8357I am Murloc!

- Join Date

- Jan 2011

- Posts

- 5,205

A 52/48 split on a non binding referendum does not a mandate make. An opinion held by 25% of the populace is not "The will of the people!". Originally Posted by Rother

Calling what is happening right now a "plan" is pretty fucking generous, there is no plan, there never was.

-

2018-11-11, 05:57 PM #8358The Lightbringer

- Join Date

- Jul 2014

- Location

- The Sunny Uplands

- Posts

- 3,825

Brexiteers like me always had a "plan". Even msm is only just now recognising how effective it most likely will be... Originally Posted by Kronik85

https://twitter.com/Peston/status/1061627934946009088

"no agreement between Weyand and Robbins by Monday night, and no approval of that agreement by cabinet on Tuesday, risk of no-deal Brexit rises very very appreciably." Robert Peston

Looks like remainers must fall back on that old saying 'cometh the hour cometh the man' and now only Vince the Cable is left to stand up and fight their corner.

Oh dear was that their plan? No wonder they lost the peoples vote a couple of years back...tick tock.13/11/2022 Sir Keir Starmer. "Brexit is safe in my hands, Let me be really clear about Brexit. There is no case for going back into the EU and no case for going into the single market or customs union. Freedom of movement is over"

-

2018-11-11, 06:01 PM #8359The Unstoppable Force

- Join Date

- Feb 2008

- Location

- pending...

- Posts

- 23,968

Wait, did you have a plan or did you have a "plan"? And what happened to either? Originally Posted by dribbles

Originally Posted by ash

Originally Posted by PC2

-

2018-11-11, 06:50 PM #8360I am Murloc!

- Join Date

- Apr 2011

- Posts

- 5,021

So you are counting on the "brilliant plan" being "make ourselves look like completely incompetent idiots for two years, so that we end up with no-deal". And you are delighted by this, because it will hurt the EU. Originally Posted by dribbles

As plans go, it's right up there with "I'm going to blow my own brains out right next to this guy, because then he will get blood on his suit and have to pay for the dry-cleaning".

And you STILL don't get it. If it comes down to a choice between no-deal and either cancelling Brexit or second referendum, then no-deal doesn't have a hope. Your ONLY chance of getting any form of Brexit through is if May comes up with something so watered down that the EU and Labour would actually support it. Otherwise the Tories will be calculating whether just cancelling will be more damaging to their party, or accepting a second referendum. Because make no mistake, from day 1 Brexit has all been about preventing damage to the Tories, and a no-deal would destroy them. It would damage the economy so much it would drive them out of power for decades, and it would almost certainly split their party in two. They aren't going to do it, and the reason their bluff isn't working is that nobody believes for one second that they will.

Well, nobody except certain, ahem, special people that seem to think their fascist wet dreams are going to come true some day. So tick and tock all you like, a broken clock may be right twice a day, but that's still at least three times more than you.When challenging a Kzin, a simple scream of rage is sufficient. You scream and you leap.

Originally Posted by George Carlin

Originally Posted by Douglas Adams

Reply With Quote

Reply With Quote