Limited PvP -> PvE Free Character Transfers

Limited PvP -> PvE Free Character Transfers The Cataclysm Classic Pre-Expansion Patch Arrives April 30

The Cataclysm Classic Pre-Expansion Patch Arrives April 30 Season 4... Just old dungeons and new ilvl?

Season 4... Just old dungeons and new ilvl? [WeakAura] Tombstone's Conditions

[WeakAura] Tombstone's Conditions Did Blizzard just hotfix an ilvl requirement onto Awakened LFR?

Did Blizzard just hotfix an ilvl requirement onto Awakened LFR? MMO-Champion

MMO-Champion

Called on a terrible definition, revert to rhetoric. :yawn:Originally Posted by Cybran

Recent Blue Posts

Recent Blue Posts

Recent Forum Posts

Recent Forum Posts

-

2015-03-16, 04:33 PM #34721Banned

- Join Date

- Jan 2011

- Location

- Mini Soda

- Posts

- 30,509

-

2015-03-16, 04:33 PM #34722Deleted

Cybran is joking when he doesnt break it up into competive consumer goods and well raw materials.

Iam pretty sure the extreme number for canda is due to oil or some sheanigans.

-

2015-03-16, 04:34 PM #34723Banned

- Join Date

- Sep 2011

- Posts

- 11,829

It is NEGLIGIBLE when compared to the benefitted liquidity that American banks will get from the capital flight from EU. Originally Posted by Rukentuts

-

2015-03-16, 04:35 PM #34724DeletedI bet with you that the US isnt happy about the weak euro. Originally Posted by Cybran

-

2015-03-16, 04:35 PM #34725Banned

- Join Date

- Jan 2011

- Location

- Mini Soda

- Posts

- 30,509

So now we're combining the terrible subjective definition with rhetoric. Originally Posted by Cybran

-

2015-03-16, 04:37 PM #34726Deleted

Cybran knows his 2nd favorite hobby after bashing the US is blaming germany so he knows that the US complains about the undervalued Euro.

That is if the can muster the memory span.

-

2015-03-16, 04:43 PM #34727Banned

- Join Date

- Jan 2011

- Location

- Mini Soda

- Posts

- 30,509

Kim Jong Un has a 100% approval rating, so Putin has something to work on. Originally Posted by Kangodo

-

2015-03-16, 04:48 PM #34728DeletedThe puppet switch term limit bypass if not the voting manipulations make him that and of cource international independent bodys agree. Originally Posted by Kangodo

-

2015-03-16, 04:49 PM #34729Banned

- Join Date

- Jan 2011

- Location

- Mini Soda

- Posts

- 30,509

No, his authoritarianism as documented by Western scholars is just all part of a grand conspiracy. Originally Posted by Kangodo

-

2015-03-16, 04:54 PM #34730Banned

- Join Date

- Jan 2011

- Location

- Mini Soda

- Posts

- 30,509

Proof his popularity means jack shit. Russians apparently don't care about having basic first-world rights if it means annexing a peninsula and another recession now and again. Originally Posted by Kangodo

-

2015-03-16, 04:57 PM #34731Banned

- Join Date

- Jul 2013

- Location

- Bank of the Columbia

- Posts

- 20,935

The EU exports more to Switzerland (~$308 billion), a country of 8 million, than to Russia (~$219 billion) a country of 144 million, despite both sharing land boarders with the EU. Originally Posted by Cybran

-

2015-03-16, 05:01 PM #34732Banned

- Join Date

- Jan 2011

- Location

- Mini Soda

- Posts

- 30,509

Depends on what you mean by "fake". Are the numbers themselves fake, or are the people deluded enough to not care? Originally Posted by Kangodo

- - - Updated - - -

How negligible. Originally Posted by Kellhound

-

2015-03-16, 05:02 PM #34733DeletedYou're overestimating what Western propaganda can do to Russians. They're now more anti-West than ever before. Trans-Atlantic idiots are hated now more than ever before - and they're getting rid off at the same time. Originally Posted by Cybran

After Putin, there will be more aggressive leader.

-

2015-03-16, 05:03 PM #34734Banned

- Join Date

- Jan 2011

- Location

- Mini Soda

- Posts

- 30,509

To not give a shit that your autocratic ruler is assassinating opposition, and stripping away basic rights, requires a significant amount of delusion. Originally Posted by Kangodo

-

2015-03-16, 05:04 PM #34735DeletedMore agressive leader would be too stupid to walk the line and hit a brick wall fast. Originally Posted by b2121945

See we dont have a termlimit either but once its in place you dont bypass enshrined rules with a puppet switch. Originally Posted by Kangodo

-

2015-03-16, 05:05 PM #34736DeletedPlease, let's not hate the whole continent because of one lunatic state. Originally Posted by Kangodo

-

2015-03-16, 05:06 PM #34737Banned

- Join Date

- Jan 2011

- Location

- Mini Soda

- Posts

- 30,509

Freedom of speech, press, assembly, voting... Originally Posted by Kangodo

The latter of which I am 107% sure of.

-

2015-03-16, 06:15 PM #34738DeletedThere is a plan, desperation trying to stop the clock. Originally Posted by Djalil

Trying to perpetuate the 20th century post-cold war status quo into the 21st century, "full spectrum dominance" "make sure nobody can oppose the US" and all that nonsense, as if it's in any way possible to hold back progress. They can hit the breaks to slow down, but the course is set and it is no stopping the future of the multi-polar 21st century world. All this meddling is why the US is the enemy of the 21st century.

-

2015-03-16, 06:16 PM #34739Deleted

I have an idea for peacefull coeexistence for Russia.

Stop quoting german wartime propaganda about poland replacing poland with ukraine.

Seriously I watched a documetary some minutes ago and its the same shit about protecting ethnic minoritys and getting them back into the home country.

It might be possible that there are a very limit number of good rationals to justify outright imperialist behaviour and wars of agression thought.

However its no excuse and glad that Russia has lost most positive diplomatic sway they once had in the east for decades to come.Last edited by mmocd79acbf389; 2015-03-16 at 06:23 PM.

-

2015-03-16, 06:24 PM #34740Banned

- Join Date

- Sep 2011

- Posts

- 11,829

I had to check the local store to see if they had Bloodborne. Originally Posted by Davillage

http://ftalphaville.ft.com/2015/03/1...ion-of-europe/

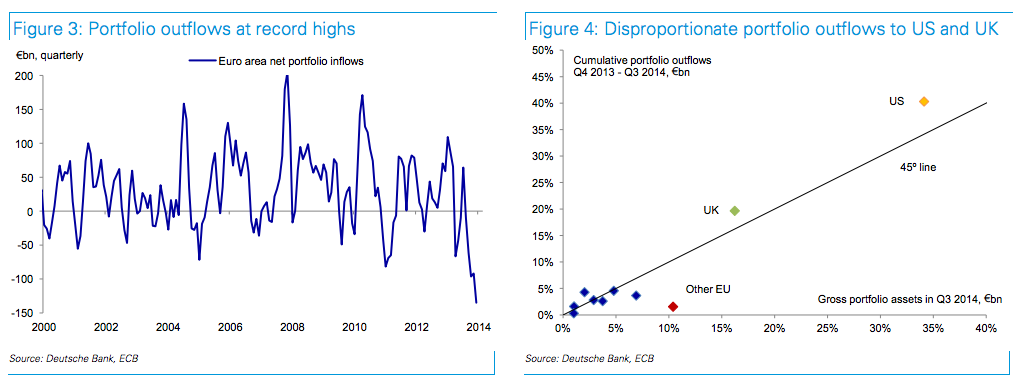

The large current account surplus combined with ECB easing and negative rates has initiated a process of large-scale capital outflows from Europe. In the second half of 2014, the euro area saw record net investment in foreign portfolio assets, reaching €135bn in Q4 (Figure 3), or around half a trillion in annualized terms. There are no indications that this trend has reversed or slowed down since. More than 90% of these flows are attributable to fixed income, though equity outflows accelerated markedly in December. At the same time, ‘other investment’ outflows- –mostly bank lending in the European periphery—have diminished relative to the financial account. The expansion of the Eurozone’s financial account has thus been driven by portfolio outflows. This stands in stark contrast to the pre-crisis decade, during which the Eurozone recycled its intermittent and meager surpluses through EUR-denominated loans to the European periphery.

Portfolio outflows from the euro area have been searching for yield overseas. Relative to the allocation of the EMU’s total stock of foreign portfolio assets, recent flows have disproportionately favoured assets in the US, the UK, and Canada (Figure 4). By contrast, the rest of the European Union—Scandinavia and Eastern Europe—have seen disproportionately small outflows as a result of being drawn into the Eurozone’s disinflationary spiral. If one plotted outflows against assets at the beginning of the four-quarter period, the new investor bias towards the Anglo-Saxon countries would be even starker.

Money outflows from Europe to USA and UK will make borrowing costs there much lower and boost local consumption. The US relies on local consumption much more than it does on exports.

The same thing happened in 2010 when money fled Southern Europe and went to Germany which helped them refinance their debts and savee BILLIONS OF EURO. German exploited the situation then.